One of the least remarked features of Taiwan's AI hardware boom is that it has not been led by the kind of companies the global business press usually celebrates. There are no garage startups here, no twenty-something founders, no venture capital origin myths. The firms riding the AI infrastructure wave, supplying cold plates to GB300 racks and vapor chambers to hyperscaler servers, are for the most part middle-aged industrial companies that have been grinding away in the component trenches for three decades or more.

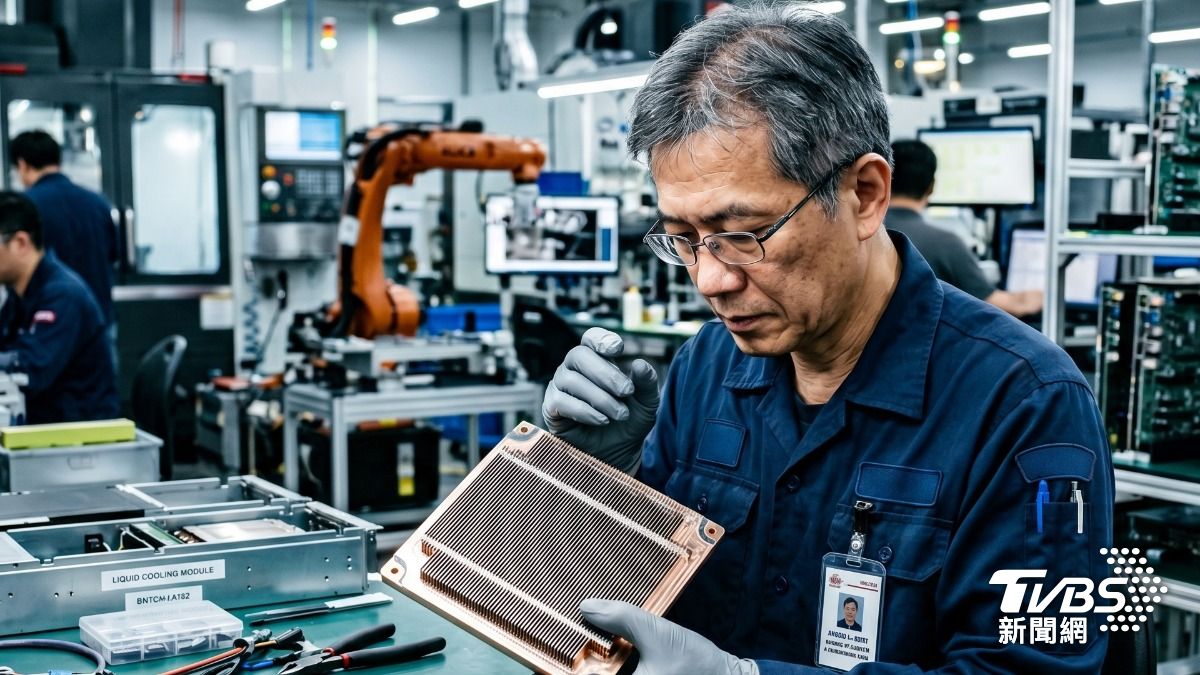

Asia Vital Components serves as the archetype. Founded in 1991 in Kaohsiung as a maker of fans and heat sinks for desktop PCs, AVC spent the first twenty-five years of its existence as a quietly competent thermal supplier, the kind of firm that showed up in bills of materials rather than headlines. AVC's 2025 revenue reached roughly US$4.5 billion, nearly double the previous year, driven largely by liquid cooling modules as well as an estimated 40-50 percent of the Nvidia GB200/GB300 cold plate market. Its chairman has called 2026 the "liquid cooling era" and is expanding cold plate, manifold, and chassis capacity in Vietnam, with a US footprint under evaluation.

The AVC story is not a sudden pivot. That is precisely the point. The company did not wake up one morning and decide to become an AI infrastructure play. It simply kept doing what it had always done, moving heat away from silicon, while the silicon itself grew dramatically hotter. When a Blackwell GPU draws over a thousand watts and a rack exceeds a hundred kilowatts, the problem stops being electrical and becomes thermal. When the upcoming Vera Rubin accelerators push GPU thermal design power to 1,800–2,300 watts and racks to 190–230 kilowatts, the problem becomes borderline civil-engineering. The companies best positioned to solve it are not the ones with the fanciest business plans but those with the deepest patent libraries in two-phase cooling, the longest relationships with ODM server builders, and the factory muscle memory to ramp a new cold plate design from prototype to volume in weeks rather than quarters. AVC alone holds more than 1,700 thermal patents. Such expertise cannot be accumulated in a Series B funding round.

This pattern echoes across the AI infrastructure supply chain. In thermal management, Auras Technology, founded in 1998 in New Taipei City as a notebook cooling specialist, spent two decades becoming the world’s largest designer of laptop heat pipes and vapor chambers before retooling for direct-to-chip cold plates and 3D vapor chambers. Its full-year 2025 revenue reached NT$23.3 billion (about US$740 million) an increase of 47%, with even stronger momentum in early 2026, including a 121.6% year-on-year jump in January. The company recently earned AMD vapor chamber certification, broadening its reach. Other veterans such as Sunon (1980), AcBel Polytech (1981), Teco Electric (1956), Cooler Master (1992), and Chenbro Micom (1983, server chassis) fill complementary niches in fans, power supplies, and systems integration. None of these names are familiar to readers of English-language tech press, yet all are now indispensable.

Taiwan’s PCB manufacturers tell a parallel story. Unimicron (1990), Nan Ya PCB (with Formosa Plastics Group lineage from the 1970s), Zhen Ding Technology (2006), Compeq (1973), and Elite Material (1992) are enjoying what Unimicron’s chairman has called a “golden decade.” A single AI server consumes fifty to sixty times more board material than a traditional server, while the boards themselves have grown an order of magnitude more complex. Elite Material, the first supplier qualified for M9-grade copper-clad laminates, is targeting a 70% capacity increase over three years.

The pattern even extends into robotics and motion, which used to sit outside the semiconductor conversation entirely. Hiwin Technologies, founded in 1989 in Taichung, spent thirty-five years as a precision machinery firm grinding ball screws and linear guideways for machine tools and semiconductor equipment. It is now directing that expertise towards ball screws for dexterous robotic hands, servo motors for robotic torsos, and high-load planetary roller screws for humanoids, and making its first-ever appearance at Computex in 2026. Aspeed Technology, a relative newcomer at 2004, but still predating the generative-AI wave by a long way, holds roughly 70 percent of the global market in baseboard management controllers, the unglamorous "life-support" silicon that keeps high-density liquid-cooled AI racks awake. Its 2025 EPS surpassed MediaTek's.

Taiwan’s leadership in AI infrastructure hardware thus rests not on flashy algorithms or venture capital, both of which remain unremarkable by global standards, but on forty years of accumulated manufacturing excellence, precision engineering, and a dense ecosystem of mid-sized component firms nurtured by Hsinchu, Southern Taiwan, and Central Taiwan science parks. These companies were already excellent at something slightly adjacent when the AI wave arrived, and the market came to them.

This quiet lesson runs counter to much industrial policy thinking. Countries looking at the AI boom and wondering how to position themselves tend to reach instinctively for the greenfield playbook. Build an AI hub. Fund a generation of startups. Train thousands of machine learning engineers. Announce a sovereign AI strategy. None of these steps are inherently wrong, but they miss where the real compounding occurs. Countries seeking to participate in the AI build-out would do better to identify their own mature industrial clusters featuring dense networks of SMEs with deep technical know-how, tight tolerances, and long client relationships. Germany’s Mittelstand, Japan’s specialty chemicals and robotics suppliers, Italy’s machine-tool clusters, the Nordic countries’ sensors and electrification expertise, and the UK and France’s aerospace and materials networks all share Taiwan’s characteristics. Each sits one adjacent capability away from meaningful contribution to the development of world-class AI industrial infrastructure.

The most durable value often emerges from the deliberate marriage of old and new. Taiwan’s more interesting startups, as seen in the CES 2026 TTA pavilion, are increasingly presented alongside established supply-chain partners rather than as standalone ventures. A sensor company without manufacturing depth is merely a demo; a manufacturing veteran without a sharp application focus risks commoditization. Delta, AVC, Auras, Hiwin, and others are each making exactly this integration move from their respective thirty-year base camps.

The global AI economy will not be built by algorithms alone, nor by policy announcements summoning greenfield industries into existence. As Taiwan has quietly demonstrated, it will be built by the companies like AVC, Delta, Quanta, Wistron, Foxconn, Unimicron, Auras, Hiwin, and the hundreds of others that never appear in keynote slides but were already there doing the unglamorous but essential work when the wave finally arrived. The countries that matter most in the coming decade will be those that recognize their own versions of these firms and provide the capital, customer signals, and policy support to pivot their proven expertise toward AI-era demand.